Stablecoins

When people ask me what the value of crypto is, this is the first thing I talk about

Surprise, a crypto post! While I’ve taken a break from writing about crypto, to write about general topics that I’ve been thinking about, I’ve come back to talk about stablecoins.

After more than a decade of experimentation, interestingly enough the most transformative product in crypto might also be its least glamorous. It isn’t a new blockchain or a speculative token. It’s the digital dollar. Stablecoins have quietly become the first cryptocurrency that millions of people actually use. They aren’t trying to replace the dollar; they’re simply making it move better.

Crypto began with the ambition to reinvent money. But most people don’t want new money. They want a version of the existing one that works faster, costs less, and doesn’t break when they cross a border. The dollar already holds the world’s trust. But, to me, stablecoins just gives it a new form, a form that allows the dollar to transport at the speed of the internet.

The Problem They Solve

Money today still moves as if it were chained to paper. Sending funds across borders takes days. Small businesses surrender a few percent of every sale to card networks. In many parts of the world, currencies lose value faster than people can earn them. These aren’t theoretical problems. They’re daily frustrations that shape how people live and work.

Stablecoins fix this without asking anyone to believe in a new ideology. They make money behave like information: instant, global, and almost free to send. For a family wiring money home, a shop owner paying suppliers, or a developer building in Lagos or Buenos Aires, stablecoins are not about speculation. They’re about access and control.

How Stablecoins Work

A stablecoin is a digital token designed to hold its value at one U.S. dollar. Behind every token sits a real dollar in reserve, typically held in cash and short-term U.S. Treasuries. When someone buys a stablecoin, new tokens are issued and matching dollars are added to the reserve. When they redeem, the reverse happens: tokens are destroyed and the dollars are released.

This one-to-one backing keeps the price stable. Unlike other cryptocurrencies that depend on belief, stablecoins depend on collateral and transparency. Issuers like Circle and PayPal publish reports verifying that every token is fully backed, giving users the confidence that redemption is always possible.

In practice, a stablecoin functions like digital cash. It can be stored in a phone wallet, sent anywhere in seconds, and used across a growing ecosystem of apps. What email did for messages, stablecoins are beginning to do for money.

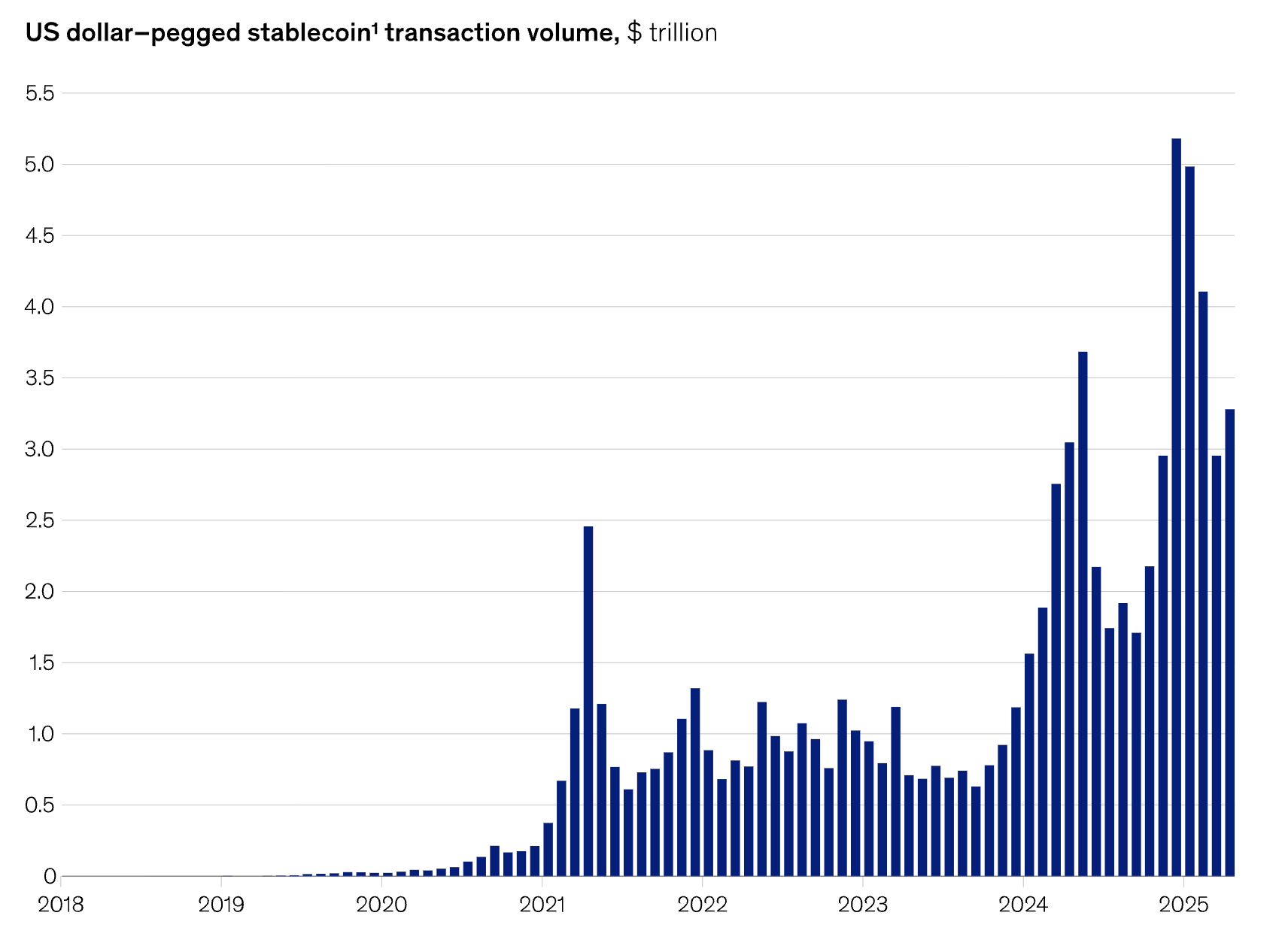

The Scale of Adoption

What started as a niche experiment has become one of the largest financial networks in the world. Stablecoins now settle more than 18 trillion dollars in transactions each year, more than Visa and Mastercard combined.

Source: Artemis; “Stablecoin surge: Here’s why reserve-backed cryptocurrencies are on the rise,” World Economic Forum, March 26, 2025 (Discovered in the mckinsey article linked in the bottom)

Crucially, this growth hasn’t been driven by speculation. It reflects genuine utility, in the form of payments, remittances, payroll, and treasury operations. In stablecoins, crypto has found something it has long searched for: a use case that stands on its own.

Economic conditions have helped, too. Rising Treasury yields have turned stablecoin reserves into productive assets. The same forces that have squeezed regional banks have given stablecoin issuers the ability to fund their own infrastructure sustainably. What began as a breakeven service has become a self-reinforcing system, where yield supports innovation rather than extraction.

The Merchant Opportunity

For merchants, stablecoins represent a quiet revolution in the cost of doing business. Card networks still take two to three percent of every transaction, often the second-largest expense after payroll. Stablecoins can lower those fees close to zero, allowing small businesses to keep more of what they earn and settle transactions instantly rather than waiting days for funds to clear.

Fintech companies see the same opportunity. Stripe, Shopify, and others are experimenting with stablecoin payments not because it’s trendy, but because it’s efficient. If consumers can keep paying with the same cards while merchants settle over stablecoin rails, adoption could spread without anyone noticing the switch. It’s the kind of backend transition that defines every major technology shift. Invisible at first, but then inevitable.

A Global Phenomenon

The most powerful story, though, is happening outside the United States. In Argentina, El Salvador, Nigeria, Turkey, and dozens of other countries, people use stablecoins to protect their savings from inflation and to transact in an economy that doesn’t trust its own banks. For them, stablecoins are not an experiment. They’re a lifeline.

More than half of stablecoin users now live outside the U.S., and the reasons are simple. They offer access to the dollar, global markets, and a stable store of value without requiring permission. In doing so, they extend American monetary influence in ways traditional banks never could: through open networks instead of closed systems. The dollar is spreading not by treaty or trade, but by code.

The Bridge to Everyday Use

Stablecoins are the first bridge between traditional finance and crypto that everyday people can cross without hesitation. They are familiar, stable, and useful on day one. You don’t need to care about blockchains to appreciate instant payments or to value stability.

This is what mass adoption will look like. Stablecoins lower the barrier without changing what people believe in. They’re not about replacing the financial system; they’re about repairing it. Governments are starting to catch up, defining how reserves must be held and how consumers should be protected. With this clarity, institutions can build confidently. And as Treasury yields provide steady income to issuers, the ecosystem gains the resources to mature responsibly.

The Next Layer

Once stablecoins become the default settlement layer, the rest follows naturally: on-chain credit, automated payroll, cross-border trade finance, and machine-to-machine payments (Check out x402, one of the teams I hope to join when I go back to Coinbase!). Each of these builds on the same foundation of a universal, programmable dollar that moves as easily as data.

Stablecoins turn money into software. They make the financial system interoperable in a way it has never been before. For the first time, anyone, from a developer to a sovereign, can build directly with money rather than around it.

The Path Forward

Skeptics often say stablecoins are just PayPal with extra steps. That misses the point. PayPal is a company. Stablecoins are a protocol. They aren’t competing with banks; they’re rewiring the rails underneath them.

The transition will be gradual, then sudden. Fintechs will integrate stablecoins behind the scenes (Stripe, Blackrock). Merchants will settle payments instantly. Consumers will still see “USD” on their screens, unaware that the infrastructure beneath has changed. The dollar will remain the dollar, only faster, more open, and available to anyone with an internet connection.

Stablecoins are not a sideshow. They are the foundation of crypto’s relevance. For all the talk of decentralization and digital assets, this is where the technology finally meets the real world. Most people don’t need a new financial system; I think they just need one that treats them better.

Crypto has promised freedom for years. Stablecoins deliver it quietly, one transaction at a time. When the story of mass adoption is written, i don’t think it will/should begin with speculation. It will begin with stability.

Helpful links:

Mckinsey Deep Dive (as much as I shit on consulting, they make really pretty graphics!)

Really great thought piece from Haun Ventures

Two goats in the crypto space explain stablecoins on the a16z podcast